- This topic has 0 replies, 1 voice, and was last updated 2 years ago by

.

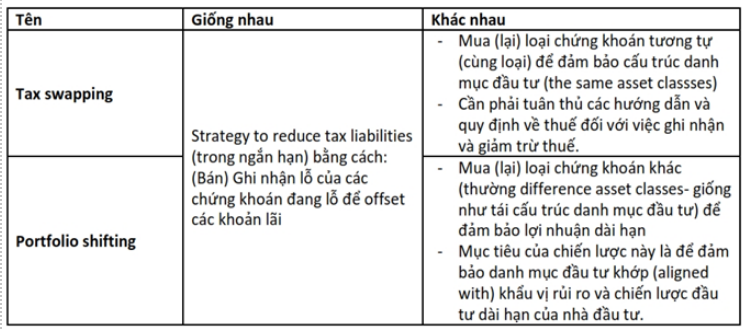

FRM2. LR: sự khác nhau giữa tax swapping và portfolio shifting

Viewing 1 post (of 1 total)

You must be logged in to reply to this topic.

You must be logged in to reply to this topic.